Wildfires in the U.S. have become more common and catastrophic than ever before. Citizens, local governments and the $2.2 trillion property and casualty insurance industry continue to be caught by surprise due to the severity and frequency of these events. So far in 2018, California alone has lost over 800,000 acres to fire, 250% more than the same period in 2017. Last year was the worst wildfire season in California history. An intense series of fires in Northern California destroyed more than 200,000 acres and killed 44 people.

With significant urban damage, 2017 also saw global insured losses from wildfires reaching a record $14 billion. Global losses from catastrophic events such as hurricanes and floods have steadily increased over the past decade, but wildfire-related losses in 2017 completely blindsided the property and casualty insurance industry.

The Problems With Current Risk Modeling Solutions

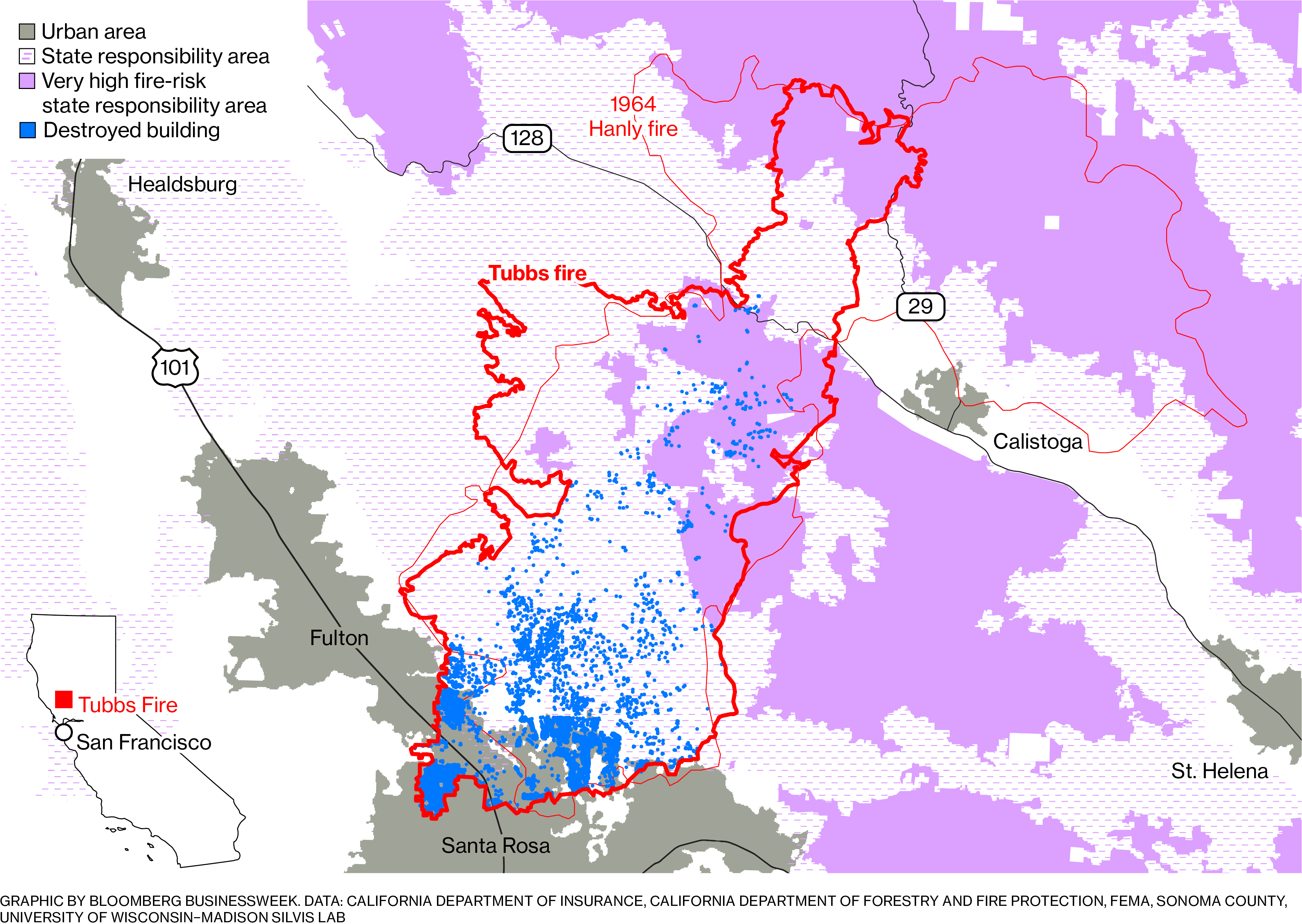

Insurance companies rely on third-party wildfire risk models and maps produced in the early 2000s to assess the risk of homes to the threat of wildfire. However, in 2017, these models performed poorly: The vast majority of buildings that were destroyed were not classified as high risk on California’s Fire Hazard Zone Map. These maps simply do not take into account individual homeowners’ situations: clearance from brush and vegetation, the use of fire-resistant construction materials, use of firebreaks or certain meteorological conditions such as wind strength and direction, etc. One home in a city or zip code may have a very different risk profile of one that is only a few blocks away. Maps don’t get refreshed often, although input characteristics, such as vegetation quality and size, frequently change.

{kind=link}